Starlink Closes Q4 2025 with 91,991 Subscribers as Satellite Internet Reshapes Nigeria’s ISP Market

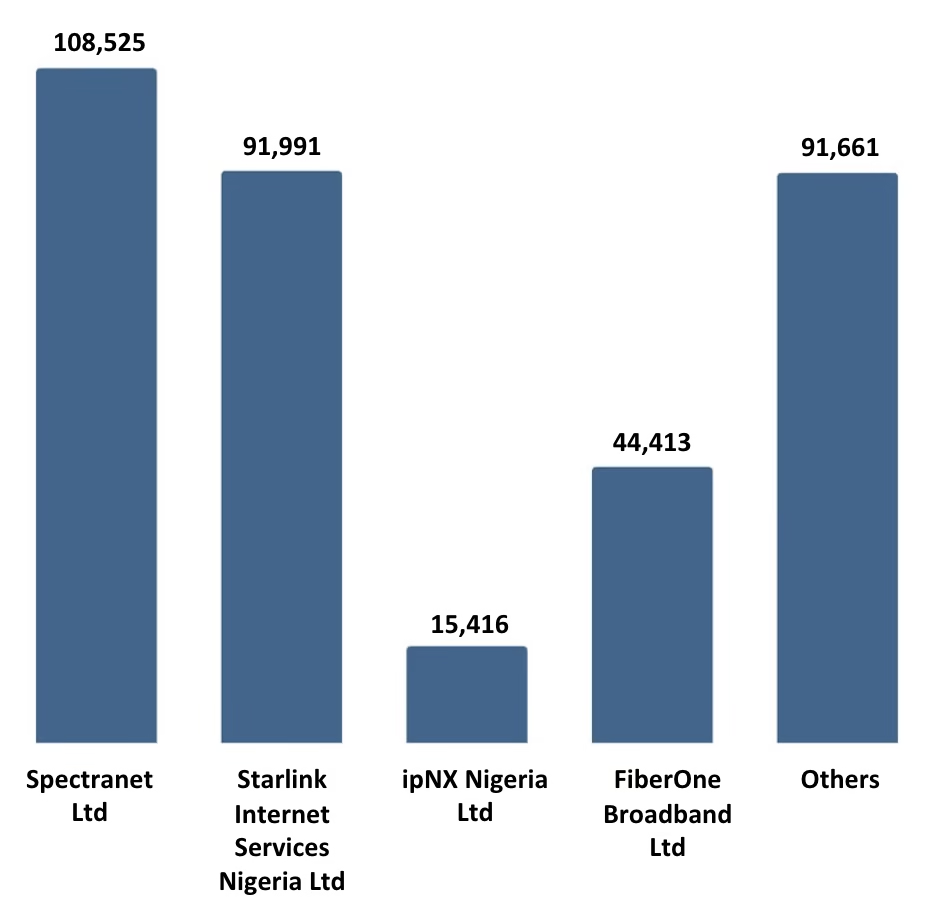

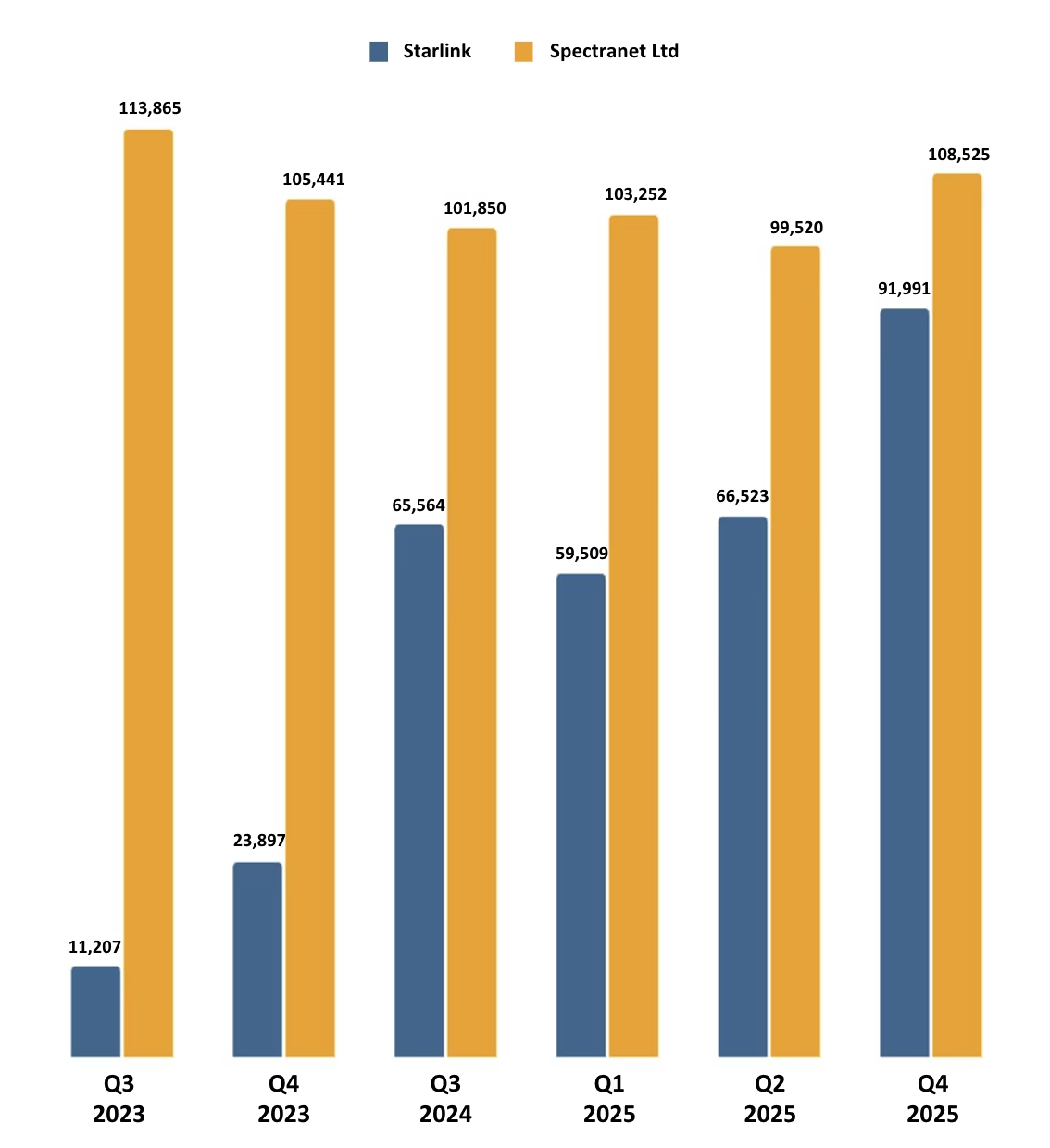

Starlink Internet Services Nigeria Ltd ended the quarter with 91,991 subscribers, narrowing the gap with long-time market leader Spectranet Ltd to 16,534, a competitive distance that stood at nearly 40,000 just five quarters earlier. Furthermore, Nigeria’s total active ISP subscriber base reached 352,006 across 2,508 points of presence in Q4 2025, up from 313,713 recorded in Q2 2025. The figures, drawn from the Nigerian Communications Commission (NCC) subscriber statistics for Q4 2025, reveal a market undergoing structural realignment, with satellite internet now operating as a primary competitive force rather than a supplementary connectivity option.

Starlink’s Sustained Ascent

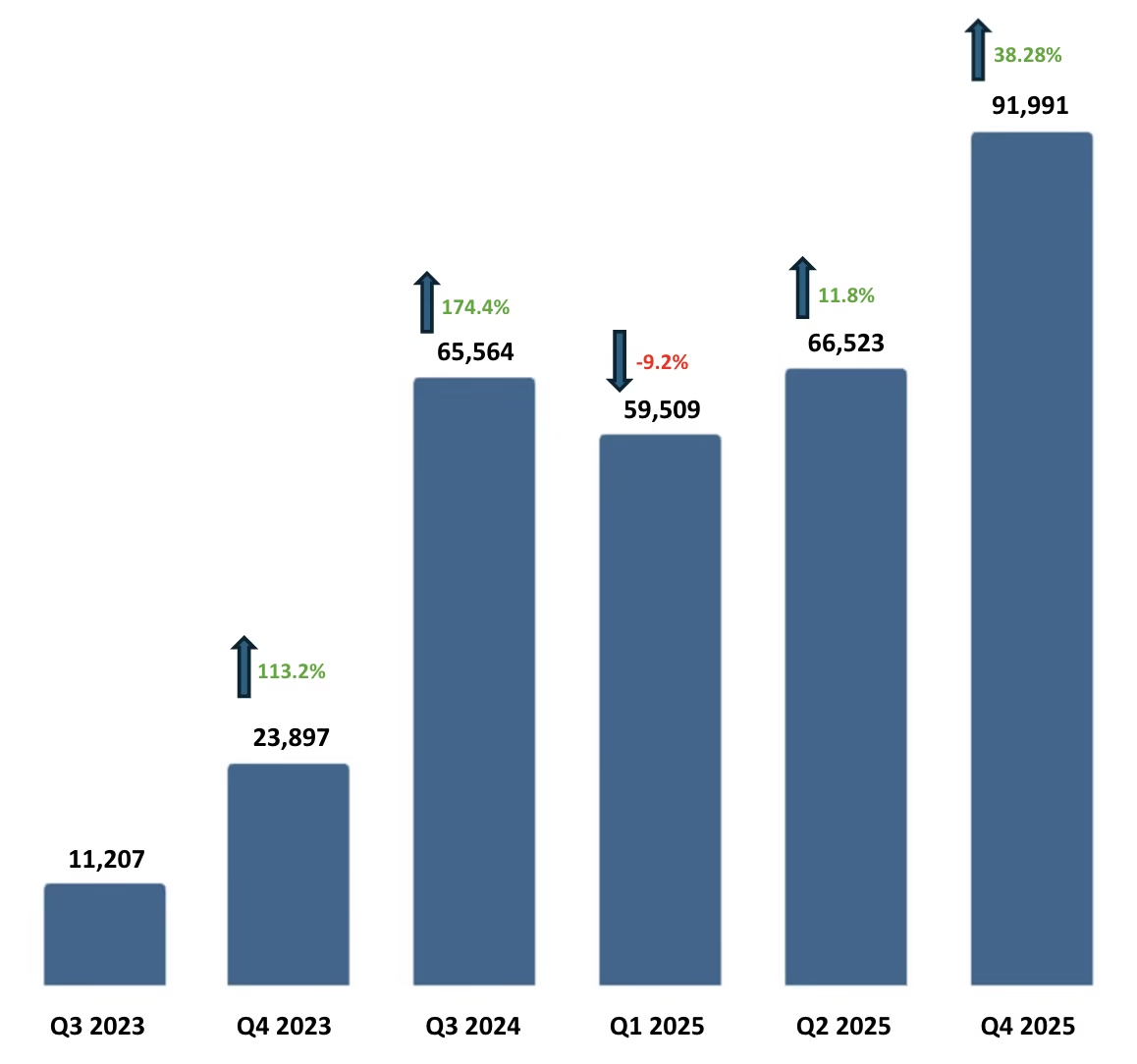

The jump to 91,991 by Q4 2025, a gain of 25,468 subscribers from Q2 alone, indicates that Starlink resolved, at least in part, the capacity constraints that had previously suppressed new registrations in high-demand urban markets, thereby converting accumulated demand into active subscriptions. That gain alone exceeds FiberOne’s entire subscriber base at its Q3 2024 peak.

The trajectory is not one of steady linear growth. Starlink fell from 65,564 subscribers in Q3 2024 to 59,509 in Q1 2025, a 9.2% decline driven by a price increase from NGN 38,000 to NGN 57,000 per month and capacity constraints that blocked new registrations in Lagos, Abuja, Abeokuta, Warri, and Benin City. The Q2 2025 recovery to 66,523 restored lost ground. The Q4 2025 growth represents a 38.3% increase in two quarters, the sharpest growth Starlink has recorded in this market.

Remote workers, SMEs, and heavy internet users with limited tolerance for service inconsistency have consistently absorbed premium pricing in exchange for reliable connectivity. As fibre and fixed wireless providers continued to face complaints about service degradation, Starlink’s value proposition strengthened rather than weakened. Whether the Q4 2025 momentum holds into 2026 depends on whether the capacity constraints that periodically suppress urban growth have been durably resolved, or whether the cycle of constraint and recovery repeats.

Spectranet’s Narrowing Lead

Spectranet ended Q4 2025 as Nigeria’s largest ISP, with 108,525 subscribers, having recovered from a low of 99,520 in Q2 2025. That recovery, ~9,000 subscribers added in the second half of 2025, has not restored competitive distance from Starlink.

Spectranet’s structural challenge is technological. As a fixed LTE provider, it operates a network architecture more susceptible to congestion in high-density areas than either fibre or satellite alternatives. Its 638 points of presence (PoP) represent the largest physical footprint among Nigeria’s top ISPs, but this breadth of infrastructure has not translated into subscriber growth in a market that increasingly rewards service quality over coverage density. Without a clear path to a technology upgrade, the compression of its lead over Starlink is likely to continue regardless of quarterly fluctuations.

FiberOne’s Consolidation

FiberOne Broadband Ltd ended Q4 2025 with 44,413 subscribers, confirming that its Q2 2025 recovery to 37,117, from a catastrophic low of 19,000 in Q1 2025, was not a temporary bounce. The Q4 figure exceeds FiberOne’s Q3 2024 peak of 33,010 by 34.5%, placing the company at its strongest recorded position in available NCC data.

However, relative to Starlink, FiberOne’s growth rate tells a different story. Between Q2 and Q4 2025, Starlink added 25,468 subscribers; FiberOne added ~7,296. Starlink now holds more than double FiberOne’s subscriber count. Fibre infrastructure scales differently from satellite; higher per-subscriber deployment costs constrain the pace of expansion, but the data confirm that in Nigeria’s current market conditions, satellite internet is outpacing fixed alternatives in raw subscriber acquisition velocity by a significant margin.

The “Others” Segment: Where 91,661 Subscribers Actually Sit

The 91,661 subscribers outside the top four operators represent 26% of Nigeria’s total active ISP subscriber base, larger than FiberOne and ipNX combined. However, this segment is not evenly distributed.

Tizeti Network Ltd (12,189 subscribers), Broadbased Communication Ltd (10,448), VDT Communications Ltd (4,479), and Cyberspace Network Ltd (4,087) together account for ~34% of this group. The remaining 100-plus licensed operators share fewer than 60,000 subscribers among them, with the majority holding subscriber counts in the double- or low-triple digits.

This tail is structurally significant. A large number of licensed ISPs in Nigeria are operating at minimal commercial scale, likely serving niche geographic or enterprise segments, or maintaining licences without substantive subscriber acquisition activity. As the top providers continue to consolidate subscriber share, the long-term trajectory for this tail is further marginalisation unless individual operators can differentiate on geography or specialisation in ways that the national providers cannot match.

Wired vs. Wireless: The Technology Fault Line

Of Nigeria’s 352,006 total active ISP subscribers in Q4 2025, 243,608 (69.2%) are on wireless connections. Only 108,398, or 30.8%, are on wired infrastructure. This ratio defines the competitive terrain.

Starlink accounts for 91,991 satellite-based wireless subscribers. Spectranet contributes 107,254 through fixed LTE. Together they account for 82% of all wireless ISP subscribers in Nigeria. On the wired side, FiberOne’s 44,413 and ipNX’s 15,001 represent the largest concentrations of fibre connectivity, with Broadbased Communication (10,448) and Ngcom (6,456) the next largest at significantly smaller scale.

Nigeria’s ISP market is a wireless market not by deliberate design but by infrastructure default. Fibre deployment remains constrained by right-of-way challenges, last-mile economics, and deployment costs across a country of significant urban density and sprawl. The dominance of wireless reflects a market in which the infrastructure gap has shaped the technology choices available to most subscribers. Starlink competes in the dominant technology category without the ground-deployment constraints that limit every other wireless operator, and it does so at a national scale currently from a single point of presence.

Points of Presence as an Efficiency Metric

Spectranet operates 638 points of presence to serve 108,525 subscribers, ~170 subscribers per POP. ipNX operates 54 POPs for 15,416 subscribers, yielding 285 per POP. FiberOne operates 29 POPs for 44,413 subscribers, a ratio of 1,531 per POP. Starlink currently operates a single declared point of presence for 91,991 subscribers.

The Starlink figure is not directly comparable in conventional infrastructure terms; its POP reflects satellite ground infrastructure rather than distributed access points. But that distinction is the analytical point. Starlink’s architecture eliminates the relationship between physical infrastructure density and subscriber reach that constrains every other operator in this market. While FiberOne must deploy fibre to each serviceable location and Spectranet must maintain tower and base station infrastructure across hundreds of sites, Starlink’s marginal cost of reaching an additional subscriber in a new location is structurally lower once satellite capacity is available.

The binding constraint for Starlink is satellite capacity, which SpaceX controls through its ongoing constellation expansion, rather than exhaustive ground-level infrastructure investment. For every other operator in this market, the growth ceiling is shaped by how much physical infrastructure they can build and maintain. That asymmetry is the most consequential structural fact in Nigeria’s ISP competitive landscape.

What Starlink’s Architecture Means for Nigeria’s Connectivity Policy

Starlink’s Q4 2025 position of 91,991 subscribers served from a single ground point of presence across a country of over 240 million people directly challenges a foundational assumption of Nigeria’s connectivity policy: that expanding internet access requires proportional expansion of physical ground infrastructure.

Nigeria’s Universal Service Provision Fund and the broader national broadband plan have historically directed resources toward fibre backbone expansion, tower densification, and last-mile infrastructure deployment as the primary levers for improving connectivity. These remain necessary investments. But Starlink’s performance demonstrates that for a defined segment of the market, one with the income to absorb premium pricing and the need for consistent high-speed connectivity, satellite internet has delivered coverage outcomes that ground infrastructure programmes have not achieved at comparable speed or scale.

The policy implication is not that investment in fibre and fixed wireless should be deprioritised. It is that the regulatory and investment framework needs to account for a technology that scales nationally without proportional ground-level deployment, and that competes directly with licensed operators carrying significantly heavier infrastructure obligations. The gap between Starlink’s single POP and Spectranet’s 638 is not just a business model difference; it is a regulatory question about which obligations attach to different categories of network operators, and whether the current framework creates an uneven competitive environment that warrants reexamination.