Could an African Spaceport Be the Answer to Growing Launch Demand? (Part Two)

Our previous analysis examined Africa’s distinctive capabilities and potential role in the expanding launch services market. We assessed the growing global demand for launch services, evaluated current spaceport capacity worldwide, and identified existing gaps in the market. Building on this foundation, we analysed Africa’s strategic positioning from a technical feasibility perspective, considering key factors including equatorial proximity, available launch azimuths and flight paths, and orbital access capabilities.

Read: Could an African Spaceport Be the Answer to Growing Launch Demand? (Part One)

This analysis examines the safety considerations for African spaceports, evaluates the commercial and economic benefits of such facilities, and reviews current spaceport projects across the continent. We conclude with a forward-looking assessment of the development of launch capabilities in Africa.

Safety Favourability

Located on South Africa’s southern coastline, the Denel Overberg Test Range is exposed to strong south-easterly winds and occasional winter storms rolling in from the Southern Ocean, both of which can disrupt launch schedules and constrain safe operating windows. Although the region sits on a stable section of the Cape Fold Belt and is not prone to major seismic activity, its coastal position means that infrastructure must withstand salt-laden air, high gusts, and rapid weather shifts. These natural conditions require conservative launch planning and robust environmental monitoring to maintain safe spaceport operations.

From the perspective of modern engineering and historical records, the Malindi Spaceport offers a highly manageable and operationally secure environment. Its weather is dominated by predictable monsoon cycles (the Kusi and Kaskazi), providing mission planners with reliable “calm windows” during which sea conditions are favourable for downrange recovery operations. Seismic records over the past decade further indicate exceptional geological stability, with no tremors exceeding Magnitude 5.0, reducing both the cost and complexity of constructing resilient launchpad infrastructure. Such factors provide favourable conditions for year-round launch capability.

Spaceport operations require secure, coordinated airspace to establish Temporary Flight Restriction (TFR) zones during launches. Somali airspace (Mogadishu FIR) is classified as a high-risk zone by the FAA and EASA due to “fake controllers” and unauthorised transmissions that could compromise the integrity of launch corridors. Combined with Somalia’s political instability and limited civil aviation infrastructure, these factors complicate airspace coordination and may increase operational costs. Effective spaceport operations in the region would require robust bilateral agreements and potentially international oversight to ensure airspace security during critical launch windows.

Djibouti presents different but equally significant challenges. Its proximity to the Bab-el-Mandeb Strait, a critical maritime chokepoint with dense international shipping and military traffic, necessitates careful coordination with commercial vessels, naval operations, and overflying aircraft. Additionally, Djibouti sits on the Afar Triple Junction, a seismically active zone where three tectonic plates diverge, producing earthquakes of magnitude 5.0+ with notable frequency. Seasonal monsoon winds and occasional tropical storms further constrain launch windows and trajectory planning.

Commercial and Economic Viabilities

Market Positioning & Revenue Projections

This component assesses how a spaceport’s geographic location translates into competitive market advantages within the global launch services industry. East African spaceports compete directly with established equatorial facilities, including the Guiana Space Centre in French Guiana and Brazil’s underdeveloped Alcântara Space Centre. The equatorial advantage, which aims to reduce launch costs by 15-20% through rotational velocity benefits, positions East African facilities to capture market share in several segments, such as geostationary communications satellites (a high-value established market by revenue), with estimates indicating launches averaging USD 80-140 million per mission, and scientific missions to low-inclination or near-equatorial orbits are estimated at similar or even more base prices.

This geographic value proposition must be effectively marketed to differentiate East African facilities from competing equatorial spaceports globally, establishing clear cost and operational advantages that justify customer migration from established launch sites.

Launch Frequency Projections and Commercial Viability

Projecting launch frequency and assessing competitive positioning establishes the spaceport’s commercial valuation within the global space economy. For an African spaceport to achieve financial viability, initial projections should target 12-24 annual launches within the first five years of operation, scaling to 40-50 launches by year ten as infrastructure matures and customer relationships deepen. The global space launch services market is projected to grow from USD 14.67 billion in 2024 to USD 78.02 billion by 2035, with African spaceports poised to capture a share of this growth due to geographic advantages and competitive pricing.

The financial model should incorporate launchpad lease arrangements that allow commercial operators, both international launch service providers and African satellite operators, to access equatorial launch trajectories without bearing the full costs of infrastructure development. Revenue projections must account for both long-term facility leases and per-launch service fees. The emerging space tourism sector, projected to reach multi-billion dollar valuations by 2030, presents an additional revenue opportunity for East African spaceports. Suborbital flight operations can leverage equatorial positioning to offer consistent launch windows and unique ocean-to-orbit visual experiences. Furthermore, the region’s central geographic location positions it as a potential hub for future intercontinental point-to-point suborbital transport services.

Investment Models

Public-Private Partnership: Public-Private Partnerships (PPPs) offer a proven framework for developing capital-intensive space infrastructure without requiring prohibitive upfront government expenditure. In the context of African spaceport development, PPPs enable governments to leverage private-sector capital, technical expertise, and operational efficiency while retaining regulatory oversight and strategic control over nationally significant assets.

For spaceports specifically, this model is particularly effective, where private launch service providers bring established customer networks, proven technologies, and operational knowledge. At the same time, host governments provide access to land, regulatory frameworks, and coordination with national security and aviation authorities. This arrangement accelerates the development of launch facilities, ground support infrastructure, and tracking systems, infrastructure that would otherwise require years of public funding cycles and technical capacity building.

Private Sector Involvement: By creating favourable business environments, governments can encourage private space companies to invest in spaceport development. Companies that manufacture, test, and launch satellites can establish facilities at the spaceport to conduct their operations. Additionally, private firms can invest in space exploration activities, with the data collected made available to governments on a commercial basis.

Direct Government Investment: This will involve public funding of core spaceport infrastructure that enables commercial operations. This typically includes land acquisition, horizontal infrastructure such as roads, power systems, propellant storage facilities, and launch pad platforms, as well as vertical structures including control centres, tracking stations, and administrative facilities. Governments may also fund the development of launch systems themselves, then lease capacity to domestic and international clients for payload deployment. This approach positions the government as both an infrastructure provider and a service operator, requiring a substantial capital outlay while retaining full ownership and control of revenue from spaceport assets.

Government-to-Government Funding: Through these partnerships, African nations can collaborate with countries possessing established spaceport experience to co-develop launch infrastructure. This model typically involves bilateral or multilateral agreements in which an experienced spacefaring nation provides technical expertise, funding, and operational knowledge, while the African host nation contributes land access, geographic advantages, and regional market positioning. Community members such as Kenya, Ethiopia, and Rwanda (East African Community) could jointly fund spaceport development through tripartite agreements, sharing costs and access while positioning the facility as a regional asset serving multiple national space programmes.

Economic Value of a Spaceport

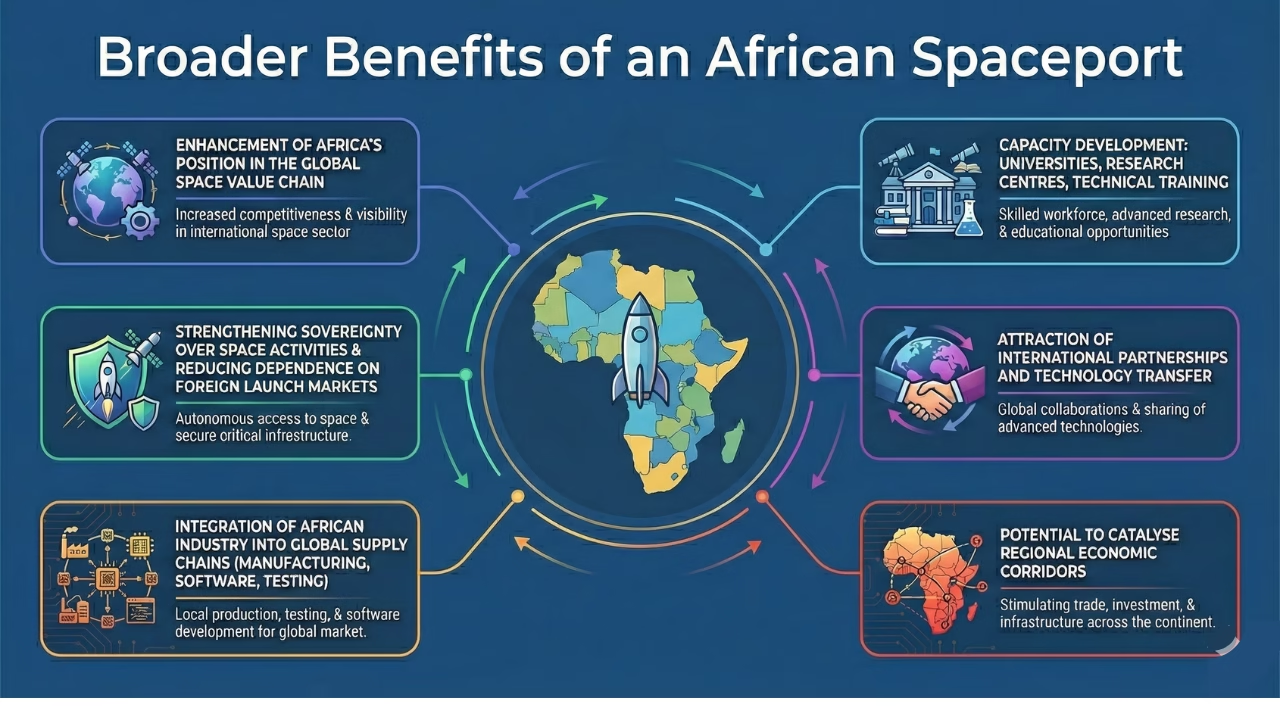

A spaceport’s value goes beyond launch operations and manufacturing, as it can also generate substantial revenue as a tourist destination. Visitors attracted to launches, space-history exhibits, and educational programmes create demand for hospitality, retail, entertainment, and services. For example, the Kennedy Space Centre Visitor Complex at Cape Canaveral draws hundreds of thousands, nearly a million, in tourists in a single year. In fiscal year 2021, its Visitor Complex alone generated about USD 148.3 million in economic output for the state, supporting roughly 1,390 jobs and contributing over USD 79.3 million in income value. An African spaceport could similarly stimulate regional tourism and employment, particularly in areas with limited industrial diversification, while showcasing African technological advancement on a global stage.

Further economic benefits include secondary economic multipliers that extend well beyond launch operations, most notably through the development of a skilled technical workforce, the emergence of specialised supply chains, and the formation of adjacent manufacturing clusters that support propulsion systems, avionics, composites, and ground-segment technologies. These activities stimulate demand for advanced engineering capabilities and reinforce national STEM education pipelines, creating a sustained flow of talent required for high-complexity aerospace work. Over time, the durability of launch infrastructure positions the spaceport as a long-term strategic asset, anchoring national space ambitions and providing a stable platform for commercial activity, innovation, and government missions across multiple decades.

Status of Spaceport Development in Africa

Djibouti

In 2023, Djibouti signed a USD 1 billion Memorandum of Understanding with Hong Kong Aerospace Technology Group (HKATG) and Touchroad International Holdings Group to build what would become Africa’s first orbital spaceport in the northern Obock region. The planned facility is to include seven satellite launch pads, three rocket‑testing platforms, and supporting infrastructure (port, power grid, roads). However, a few months later, HKATG issued a regulatory corporate announcement filed with the Hong Kong Stock Exchange (HKEX) stating that the MOU to develop a commercial spaceport in Djibouti had officially lapsed and ceased to have effect because the parties failed to sign a formal contract within the designated three-month window. Despite this expiration, the Hong Kong Aerospace Technology Group asserts that this setback will not negatively impact its financial position and that it intends to continue conducting feasibility studies for the project.

As of mid-2025, the project’s future remains uncertain. A US Congressional Research Service report on China’s engagement with Djibouti notes that whilst the plan remains officially active, the deal “faces challenges and might not proceed.”

Kenya

Under the stewardship of the Kenya Space Agency (KSA), Kenya is actively advancing the development of a Commercial Space Port in Malindi, a project designated as a priority Public-Private Partnership (PPP) within the country’s Medium-Term Plan (MTP) IV. Significant administrative milestones have already been achieved, most notably the approval of the Project Concept Note in April 2025. The focus has now shifted to procuring a Transaction Advisor (TA), with the tender having been published at the time of this analysis. Through a competitive bidding PPP procurement method, this initiative aims to build national capacity in space systems engineering and data analytics while establishing commercial launch capabilities that will drive revenue generation, employment creation, and light manufacturing of space systems.

Kenya’s spaceport potential has attracted foreign interest, notably demonstrated by the recent German NewSpace Delegation’s exploratory visit to assess investment opportunities. The delegation included several companies operating in aerospace and launch services, signalling Kenya’s emerging strategic positioning within the global commercial space sector. Additionally, Kenya hosted a delegation from China’s Oriental Space Port Research Institute (OSPRI), a prominent aerospace innovation body central to the development of the Oriental Maritime Space Port, one of China’s flagship commercial launch facilities. The engagement explored potential cooperation in commercial launch operations, satellite applications, high-resolution remote sensing technologies, and space engineering infrastructure, signalling Chinese interest in leveraging Kenya’s equatorial launch advantages through technology transfer and joint venture arrangements.

This international interest has translated into established partnerships. In May 2025, ASTRO GATE, AfriOrbit Ltd, and Hayes Group International signed a tripartite Memorandum of Understanding (MoU) to jointly promote the development of a commercial spaceport in Kenya.

South Africa

In 2025, the privately‑funded company Mura Space formalised a partnership with Aerospace Systems Research Institute (ASRI) at the University of KwaZulu-Natal (UKZN) to commercialise ASRI’s sounding-rocket launch facility at the Overberg Test Range (OTR), Arniston, Western Cape. Under this agreement, approved suborbital test launches will be permitted using both fixed and mobile infrastructure, while safety and regulatory oversight will be maintained.

Mura Space is concurrently proposing and working towards a full-fledged Mura Spaceport™, a privately funded, multi-user commercial spaceport. The Mura Spaceport™ is being designed to meet rising global launch demand, offering multiple pads and flexible scheduling to accommodate diverse vehicles and parallel missions while addressing weather and air-traffic constraints. Planning draws on lessons from international commercial spaceport challenges and identifies unique value propositions to position the facility competitively in the global launch market.

Meanwhile, interest from Elon Musk and SpaceX in using Overberg for potential orbital and polar‑orbit launches (including deployment of LEO constellations) has drawn international attention, underscoring the site’s strategic value and the potential catalytic effect on further investments.

Somalia

The Somalia Spaceport project, being advanced by Turkish Space Agency (TUA) in collaboration with the Somali government, envisages a 900 square‑kilometre launch facility along the Indian Ocean coast, exploiting Somalia’s equatorial proximity and open‑ocean launch corridor. 2025 reports indicate that construction is expected to begin shortly after a formal bidding process, with completion targeted within approximately two years. The estimated initial cost is around USD 350 million, with other estimates placing the project cost at over USD 6 billion, and significant external financial backing is a possibility.

However, the facility appears designed primarily for ballistic missile testing and military launches, which may limit or preclude its development into a commercial satellite launch spaceport.

Conclusion & Future Outlook

Africa’s spaceport ambitions present a compelling opportunity to strengthen the global launch ecosystem and position the continent as a strategic hub for rising international demand. Equatorial coastal sites offer optimal orbital access for GEO and equatorial missions, as South African launch corridors provide capability for sun-synchronous and mid-inclination LEO launches, collectively enabling distributed and resilient global launch capacity. Progress is accelerating through public-private partnerships, government-to-government collaborations, and growing private sector interest.

Economically, such spaceports can achieve viability through launch services, long-term facility leases, tourism, and future suborbital transport, while generating skilled employment, manufacturing clusters, and STEM development across the continent. Realising this potential requires overcoming regulatory bottlenecks, infrastructure gaps, and environmental constraints through strategic learning from established global spaceports and leveraging Africa’s unique geographic advantages to position the region as a competitive and essential node in the global launch network.

Looking forward, Africa’s spaceport development trajectory will likely accelerate as global launch demand outpaces existing infrastructure capacity. With mega-constellations requiring an unprecedented launch cadence and geopolitical tensions driving demand for launch-site diversity, the continent’s equatorial advantage is becoming increasingly valuable. The convergence of technological maturity, growing private sector investment, and increasing government commitment suggests that operational African spaceports could emerge within the next few decades. The question is no longer whether African spaceports will emerge, but how quickly the continent can capitalise on this window of opportunity to secure its role in the future of space access.