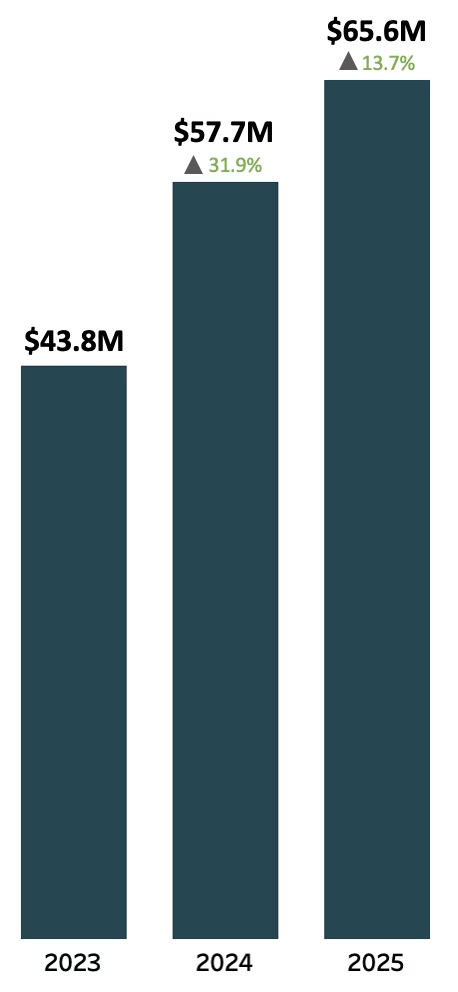

NileSat Reports USD 65.6 Million Net Profit in 2025 Despite a 2.6% Revenue Decline

The Egyptian Satellite Company (Nile Sat) delivered a year of strong headline growth in 2025, with net profit rising from USD 57.6 million in 2024 to USD 65.6 million in 2025, a 13.7% increase, reinforcing its position as a consistently profitable operator. At first glance, this suggests a company on solid footing. However, a closer examination tells a different story. The increase in profitability was driven primarily by non-operating income and favourable macroeconomic conditions, rather than core satellite operations. This is reflected in a 2.6% decline in top-line revenue, from USD 101.1 million to USD 98.4 million, signalling mounting market pressures and evolving industry dynamics. These trends underscore the need for strategic realignment to reinforce the company’s core revenue base.

Financial Performance Analysis

Core Revenue Trajectory Signals Market Pressures

Nile Sat’s declining top-line revenue was accompanied by a rise in direct operating expenses, highlighting the need for closer attention to the performance of its satellite operations. Direct operating expenses increased from USD 58.1 million to USD 59.4 million, driven primarily by satellite channels allotment costs, which grew from USD 21.1 million to USD 22.4 million. These expenses reflect agreements with other satellite operators, effectively allowing Nile Sat to borrow extra transponder capacity to provide services to its clients. As a result of lower revenues and higher costs, gross profit fell by roughly 9%, declining from USD 43.0 million to USD 39.0 million.

NileSat’s 2025 results, showing declining core revenues alongside rising operating costs, reflect broader shifts reshaping the satellite market in the Middle East and Africa. Traditional satellite TV is experiencing slower growth as viewers increasingly turn to Over-The-Top (OTT) streaming platforms, reducing demand for conventional broadcast services, which remain NileSat’s primary revenue driver. Traditional broadcast revenue streams face sustained pricing pressure, while regional operators such as Yahsat and Arabsat are actively expanding their broadband and high-speed connectivity offerings, particularly across Africa and the Middle East, to reduce reliance on legacy TV broadcast services and capture rising demand in underserved markets.

NileSat must evolve beyond traditional broadcast operations to remain competitive in a market increasingly driven by connectivity and data demand.

These competitive dynamics are further compounded by accelerating consolidation among established GEO operators, who are pursuing scale and multi-orbit integration to manage pricing pressures and optimise operating costs. The strategic logic is clear: size and orbital diversification are becoming baseline requirements for relevance in a market where LEO entrants are redefining service expectations.

Profitability Gains Driven by Non-Operational Income

Despite a decline in core operating revenue from its satellite operations, NileSat’s net profit was strongly driven by non-operational income. The company generated substantial returns from its cash reserves, earning USD 13.7 million in credit interest and USD 16.4 million from gains on securities, including bonds and treasury bills. Favourable currency dynamics further supported profitability, with a foreign currency re-evaluation gain of USD 1.8 million in 2025, marking a strong turnaround from the USD 9.9 million loss recorded in 2024. In addition, NileSat successfully recovered some expected credit losses, contributing a USD 1.3 million gain to the bottom line, compared with a USD 2.5 million expense in the prior year.

These results show that NileSat’s profitability has benefited significantly from favourable non-operating income, including financial and investment activities, rather than from its core satellite business, a trend that has persisted over the past two years. While this reliance boosts short-term earnings, it also exposes the company to risk, as any decline in interest rates or bond yields could significantly impact net profit. Furthermore, this underscores the need to strengthen its operational revenue to sustain growth and remain resilient in a competitive and evolving market.

Earnings Per Share and Cash Position Analysis

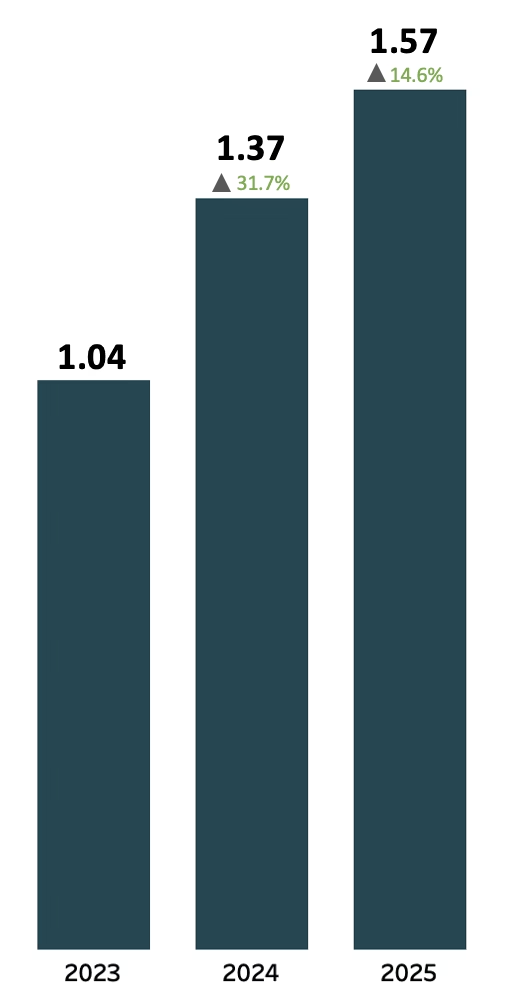

NileSat’s improved profitability is further reflected in its earnings per share, which rose from USD 1.38 in 2024 to USD 1.57 in 2025, affirming the company’s capacity to generate shareholder value even as it navigates a challenging core revenue environment. This performance is underpinned by a strong balance sheet, with the company maintaining a stable liquidity position and limited financial risk exposure.

Cash and cash equivalents rose to USD 278.5 million at the end of FY 2025, up from USD 225.3 million in 2024, a 23.6% increase, reflecting the company’s strong cash-generating capacity. This is further evidenced by total assets of USD 727.6 million, underpinned by a minimal debt load, totalling to liabilities of USD 33.7 million against owners’ equity of USD 693.9 million. This positions the company to finance strategic investments, whether in broadband infrastructure, multi-orbit capabilities, or partnerships, without material balance sheet risk.

The company demonstrates healthy cash flow, with core operations continuing to generate strong cash flows of USD 66.7 million in 2025, which easily covered the USD 18.5 million paid out in shareholder dividends. However, this position also raises a strategic question. A cash balance of USD 278.5 million against a total asset base of USD 727.6 million means that over a third of the company’s assets are held in cash or near-cash instruments. While this reflects financial prudence, it also suggests that capital is not being actively deployed toward growth. In a market undergoing the structural shifts outlined earlier, a strong cash position is only as valuable as how it is utilised to reposition the business. If left idle, it may signal caution at a time when the market demands more decisive strategic action.

African Satellite Communications Ecosystem Analysis

The financial trends observed at NileSat reflect broader dynamics within the African satellite communications market, characterised by growing demand for connectivity that underpins high market potential, while signalling a rapidly evolving competitive landscape. Despite these pressures, NileSat continues to maintain a strong leadership position within the African satellite landscape.

NileSat remains the most profitable African satellite operator on the continent, with top-line revenues nearly five times those of the next-leading African operator, and ranks among the top five operators in Africa by revenue as of 2025, outperforming several foreign competitors. This position is further reinforced by its high-throughput satellite, NileSat 301, which is in orbit and has expanded its coverage beyond Egypt and the Middle East into Sub-Saharan Africa, significantly broadening its addressable market.

This shift marks a market where growth is no longer defined by traditional broadcast dominance, but by the capacity to capture rising demand for connectivity and data-driven services. As competition intensifies across GEO, LEO, and multi-orbit models, operators that adapt their business models and deploy capital with strategic intent will be best positioned to capture long-term value in Africa’s evolving satellite ecosystem.

Regional GEO operators like NileSat, whose legacy business is anchored in direct-to-home (DTH) broadcasting, face mounting structural pressure from two directions. Globally, established operators are consolidating to build multi-orbit scale, while LEO entrants are aggressively targeting both enterprise and consumer broadband segments. NileSat’s revenue performance suggests it is already absorbing the effects of these forces, with pricing pressure and slowing demand in its traditional broadcasting segment pointing to a market outpacing its current business model.